Preferred Bank has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 11% to $94.70 per share while the index has gained 13.4%.

Is now the time to buy Preferred Bank, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

Why Is Preferred Bank Not Exciting?

We're cautious about Preferred Bank. Here are three reasons there are better opportunities than PFBC and a stock we'd rather own.

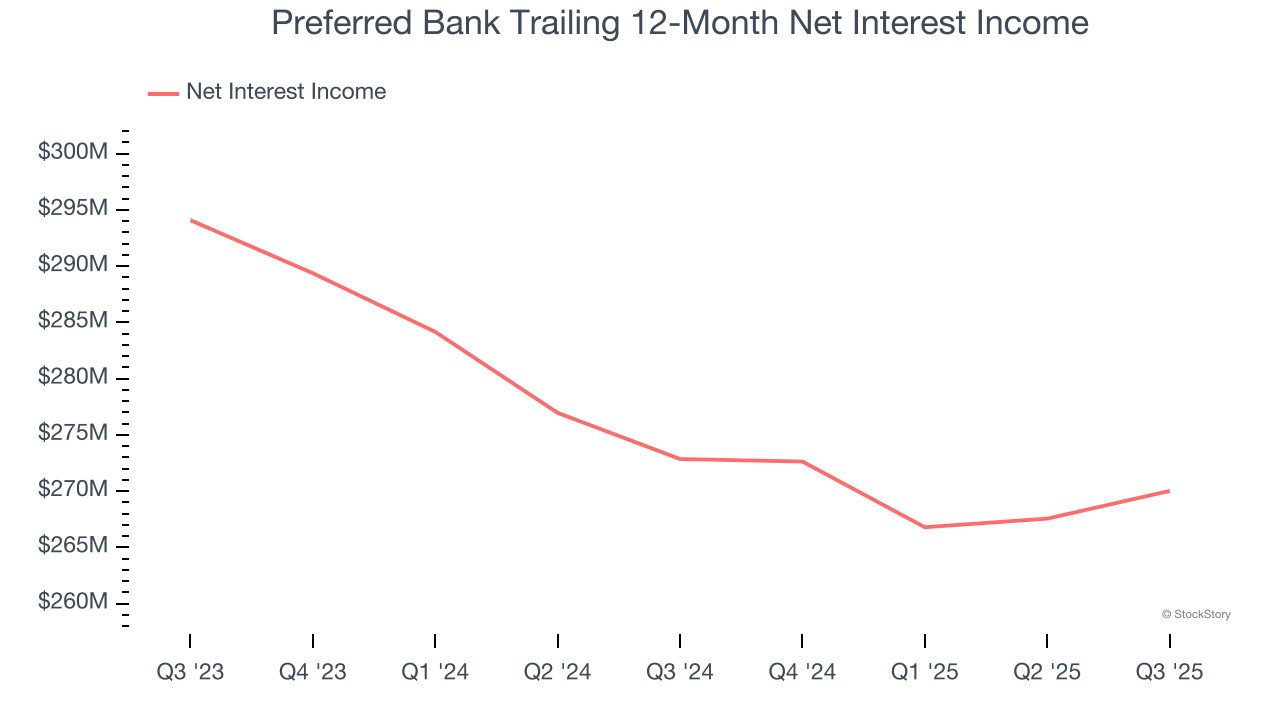

1. Net Interest Income Points to Soft Demand

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Preferred Bank’s net interest income has grown at a 9.9% annualized rate over the last five years, slightly worse than the broader banking industry and in line with its total revenue.

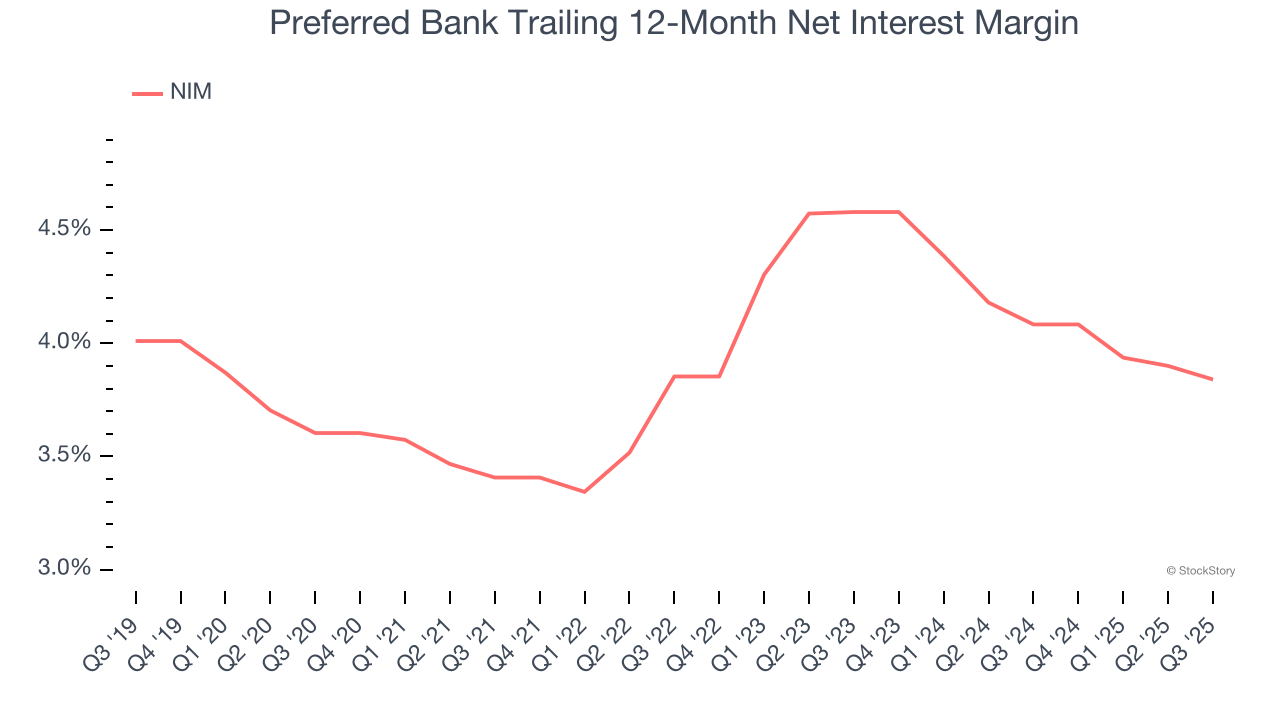

2. Net Interest Margin Dropping

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently one can generate income from its core lending activities.

Over the past two years, Preferred Bank’s net interest margin averaged 4%. However, its margin contracted by 74 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Preferred Bank either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

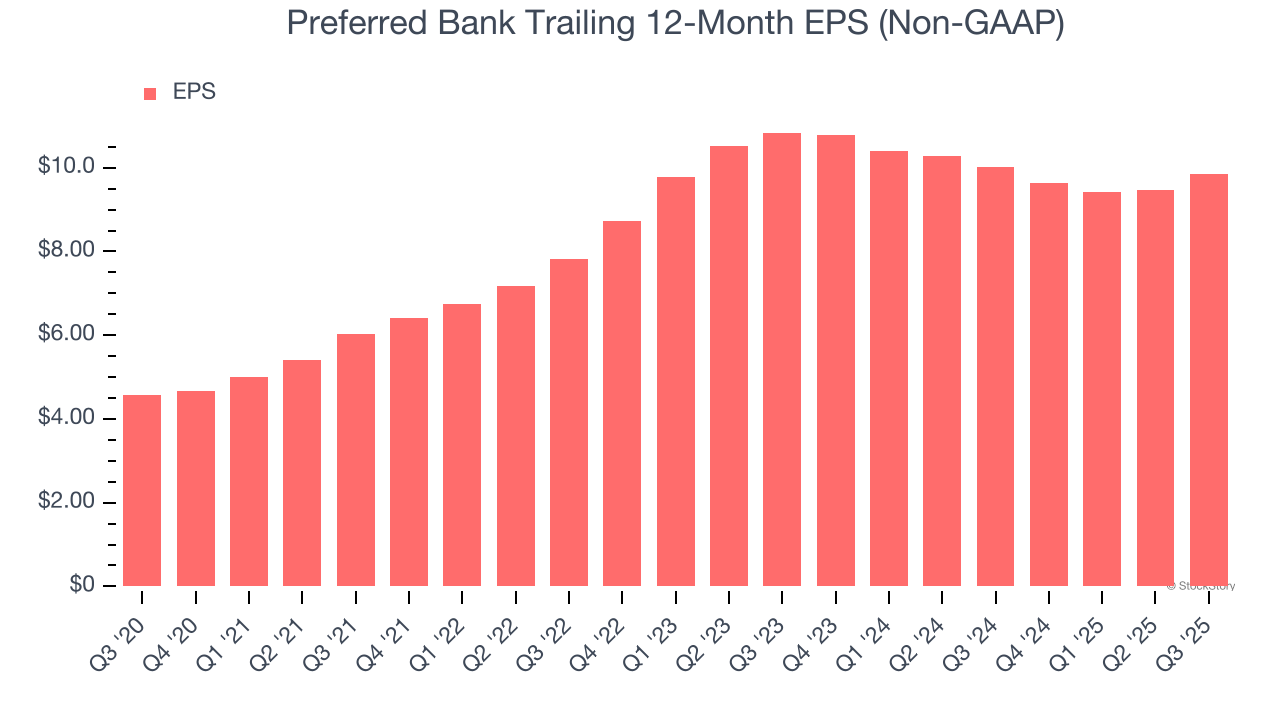

3. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Preferred Bank, its EPS and revenue declined by 4.7% and 2.8% annually over the last two years. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Preferred Bank’s low margin of safety could leave its stock price susceptible to large downswings.

Final Judgment

Preferred Bank isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 1.5× forward P/B (or $94.70 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at a top digital advertising platform riding the creator economy.

Stocks We Like More Than Preferred Bank

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.